Robust estimation methods for the mean vector, scatter matrix, and covariance matrix (if it exists) from data (possibly containing NAs) under multivariate heavy-tailed distributions such as angular Gaussian (via Tyler’s method), Cauchy, and Student’s t distributions. Additionally, a factor model structure can be specified for the covariance matrix. The latest revision also includes the multivariate skewed t distribution.

The package can be installed from CRAN or GitHub:

# install stable version from CRAN

install.packages("fitHeavyTail")

# install development version from GitHub

devtools::install_github("convexfi/fitHeavyTail")To get help:

library(fitHeavyTail)

help(package = "fitHeavyTail")

?fit_mvtTo cite fitHeavyTail

in publications:

citation("fitHeavyTail")To illustrate the simple usage of the package fitHeavyTail,

let’s start by generating some multivariate data under a Student’s \(t\) distribution with significant heavy

tails (degrees of freedom \(\nu=4\)):

library(mvtnorm) # package for multivariate t distribution

N <- 10 # number of variables

T <- 80 # number of observations

nu <- 4 # degrees of freedom for heavy tails

set.seed(42)

mu <- rep(0, N)

U <- t(rmvnorm(n = round(0.3*N), sigma = 0.1*diag(N)))

Sigma_cov <- U %*% t(U) + diag(N) # covariance matrix with factor model structure

Sigma_scatter <- (nu-2)/nu * Sigma_cov

X <- rmvt(n = T, delta = mu, sigma = Sigma_scatter, df = nu) # generate dataWe can first estimate the mean vector and covariance matrix via the traditional sample estimates (i.e., sample mean and sample covariance matrix):

mu_sm <- colMeans(X)

Sigma_scm <- cov(X)Then we can compute the robust estimates via the package fitHeavyTail:

library(fitHeavyTail)

fitted <- fit_mvt(X)We can now compute the estimation errors and see the significant improvement:

sum((mu_sm - mu)^2)

#> [1] 0.2857323

sum((fitted$mu - mu)^2)

#> [1] 0.1487845

sum((Sigma_scm - Sigma_cov)^2)

#> [1] 5.861138

sum((fitted$cov - Sigma_cov)^2)

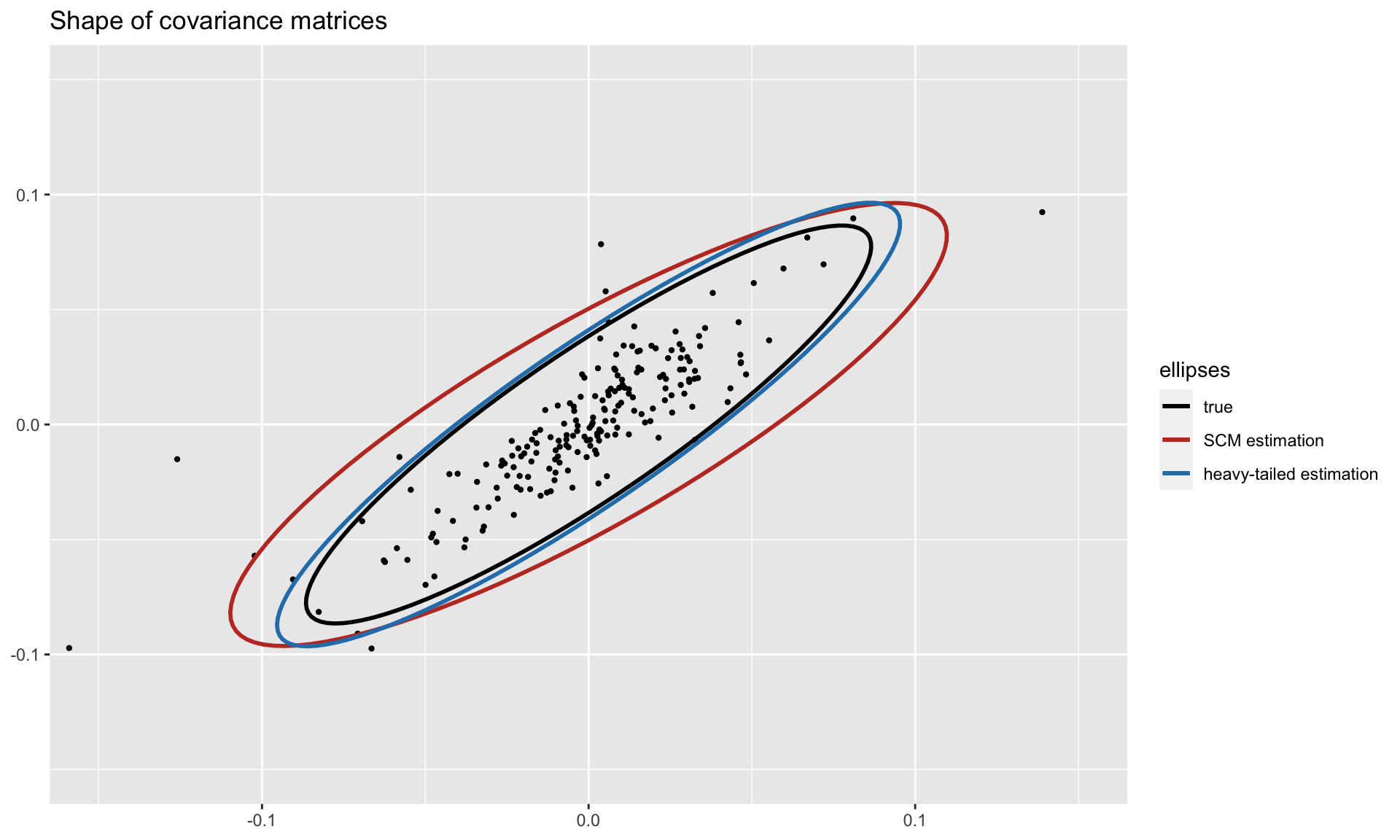

#> [1] 4.663539To get a visual idea of the robustness, we can plot the shapes of the covariance matrices (true and estimated ones) on two dimensions. Observe how the heavy-tailed estimation follows the true one more closely than the sample covariance matrix:

For more detailed information, please check the vignette.

README file: GitHub-readme.

Vignette: CRAN-vignette and GitHub-vignette.